Wazua

»

Investor

»

Stocks

»

Portfolio Balancing: Avoid Over Exposure To Financial Sector

Rank: Chief Joined: 1/3/2007 Posts: 18,390 Location: Nairobi

|

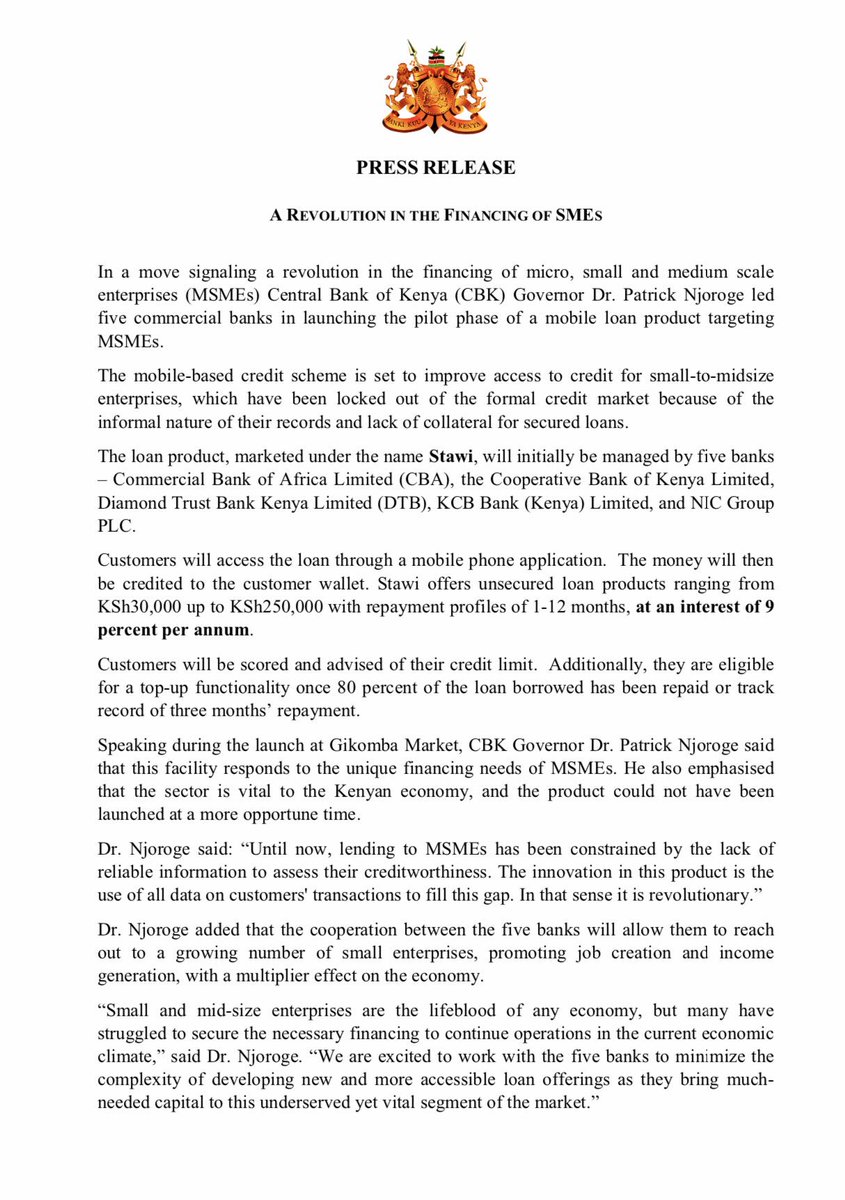

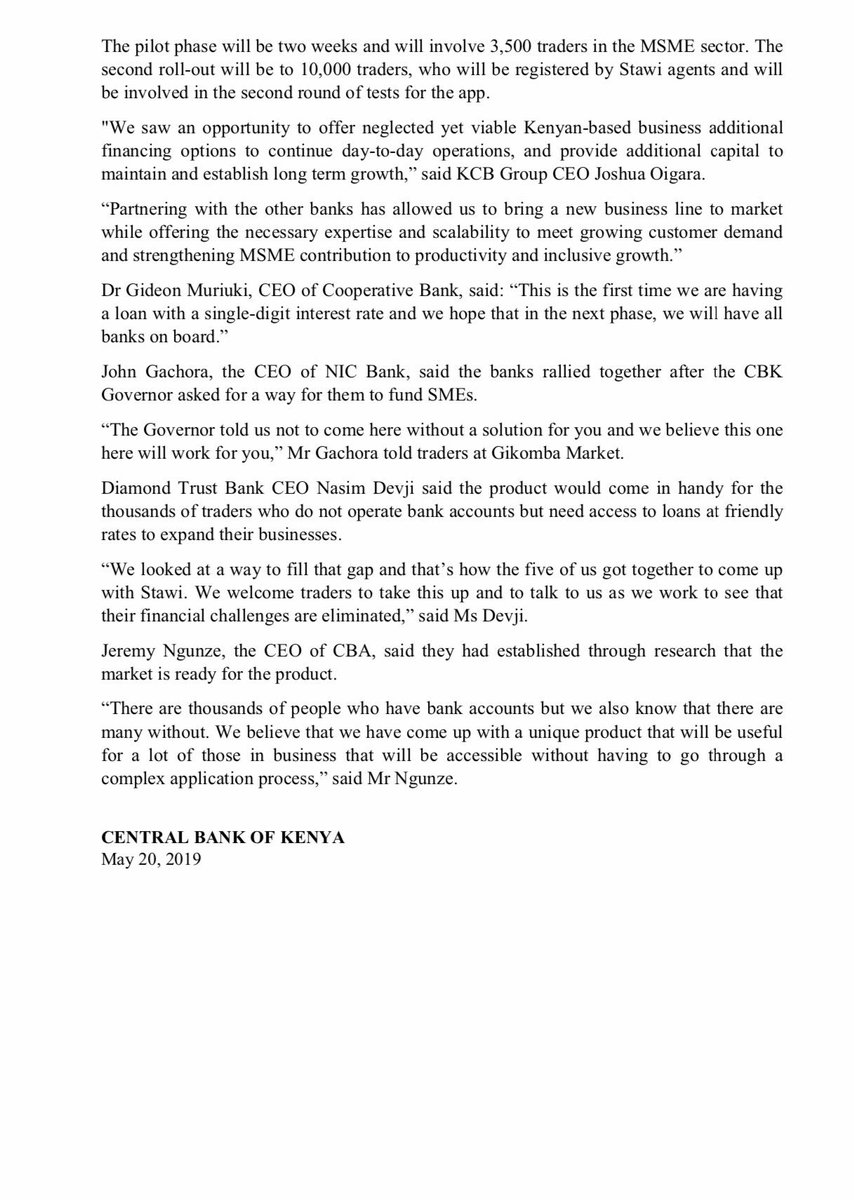

obiero wrote:VituVingiSana wrote:obiero wrote:winmak wrote:Ericsson wrote:murchr wrote:NOTICE - STAWI mobile loan facility of 30 - 250K, payable within 1 -12 months at an interest of 9% per annum   Where is equity bank and why have they been left out Unsecured!!! How have they priced in risk to lend at 9%? Or am I missing something? There are huge deposits in banks acrruing 0% interest. That’s your answer Banks can place those funds at much lower risk of default on the Interbank Market. Then there are 91 day T-Bills. Also offer secured overdrafts to existing customers. True. But the MSME market was shifting steadily to Tala,Branch etc.. It's a ring fencing strategy.. Not that banks would crumble incase they had continued ignoring the segment I do not use Tala/Branch/MShwari and the such but don't these charge rates of 3-9% per MONTH? The Stawi loans, per the press release, are at 9% per YEAR. That's lower than what they lend to AA customers. I would understand it if banks were charging 3% per month and then taking on more risk. Greedy when others are fearful. Very fearful when others are greedy - to paraphrase Warren Buffett

|

|

|

Rank: Veteran Joined: 9/18/2014 Posts: 1,127

|

winmak wrote:Ericsson wrote:murchr wrote:NOTICE - STAWI mobile loan facility of 30 - 250K, payable within 1 -12 months at an interest of 9% per annum Where is equity bank and why have they been left out Unsecured!!! How have they priced in risk to lend at 9%? Or am I missing something? Yes. Work out the APR instead. The 9% is only part of the multi layered cost structure. It is also not unsecured. The main purpose of the stock market is to make fools of as many people as possible.

|

|

|

Rank: Veteran Joined: 9/18/2014 Posts: 1,127

|

Ericsson wrote:murchr wrote:NOTICE - STAWI mobile loan facility of 30 - 250K, payable within 1 -12 months at an interest of 9% per annum Where is equity bank and why have they been left out Interesting observation. There is definitely more than meets the eye here. The main purpose of the stock market is to make fools of as many people as possible.

|

|

|

Rank: Chief Joined: 1/3/2007 Posts: 18,390 Location: Nairobi

|

If the APR is substantially higher than 13%, then is CBK backtracking on its threats that banks should have APRs that were at or lower than CBR+4? Greedy when others are fearful. Very fearful when others are greedy - to paraphrase Warren Buffett

|

|

|

Rank: Elder Joined: 6/23/2009 Posts: 14,350 Location: nairobi

|

VituVingiSana wrote:obiero wrote:VituVingiSana wrote:obiero wrote:winmak wrote:Ericsson wrote:murchr wrote:NOTICE - STAWI mobile loan facility of 30 - 250K, payable within 1 -12 months at an interest of 9% per annum Where is equity bank and why have they been left out Unsecured!!! How have they priced in risk to lend at 9%? Or am I missing something? There are huge deposits in banks acrruing 0% interest. That’s your answer Banks can place those funds at much lower risk of default on the Interbank Market. Then there are 91 day T-Bills. Also offer secured overdrafts to existing customers. True. But the MSME market was shifting steadily to Tala,Branch etc.. It's a ring fencing strategy.. Not that banks would crumble incase they had continued ignoring the segment I do not use Tala/Branch/MShwari and the such but don't these charge rates of 3-9% per MONTH? The Stawi loans, per the press release, are at 9% per YEAR. That's lower than what they lend to AA customers. I would understand it if banks were charging 3% per month and then taking on more risk. How will banks charge more than the rate cap directive.. The only way is to go lower to stem the tide. MSME have no issue with loans as high as 23% per annum but the law restricts! COOP, IMH, KEGN, MTNU

|

|

|

Rank: Chief Joined: 1/3/2007 Posts: 18,390 Location: Nairobi

|

obiero wrote:VituVingiSana wrote:obiero wrote:VituVingiSana wrote:obiero wrote:winmak wrote:Ericsson wrote:murchr wrote:NOTICE - STAWI mobile loan facility of 30 - 250K, payable within 1 -12 months at an interest of 9% per annum Where is equity bank and why have they been left out Unsecured!!! How have they priced in risk to lend at 9%? Or am I missing something? There are huge deposits in banks acrruing 0% interest. That’s your answer Banks can place those funds at much lower risk of default on the Interbank Market. Then there are 91 day T-Bills. Also offer secured overdrafts to existing customers. True. But the MSME market was shifting steadily to Tala,Branch etc.. It's a ring fencing strategy.. Not that banks would crumble incase they had continued ignoring the segment I do not use Tala/Branch/MShwari and the such but don't these charge rates of 3-9% per MONTH? The Stawi loans, per the press release, are at 9% per YEAR. That's lower than what they lend to AA customers. I would understand it if banks were charging 3% per month and then taking on more risk. How will banks charge more than the rate cap directive.. The only way is to go lower to stem the tide. MSME have no issue with loans as high as 23% per annum but the law restricts! KCB and CBK loans via MShwari have APRs higher than 50%. The APR includes fees so a facilitation fee of 7% per month is more than 90% APR. Greedy when others are fearful. Very fearful when others are greedy - to paraphrase Warren Buffett

|

|

|

Rank: Elder Joined: 6/23/2009 Posts: 14,350 Location: nairobi

|

VituVingiSana wrote:obiero wrote:VituVingiSana wrote:obiero wrote:VituVingiSana wrote:obiero wrote:winmak wrote:Ericsson wrote:murchr wrote:NOTICE - STAWI mobile loan facility of 30 - 250K, payable within 1 -12 months at an interest of 9% per annum Where is equity bank and why have they been left out Unsecured!!! How have they priced in risk to lend at 9%? Or am I missing something? There are huge deposits in banks acrruing 0% interest. That’s your answer Banks can place those funds at much lower risk of default on the Interbank Market. Then there are 91 day T-Bills. Also offer secured overdrafts to existing customers. True. But the MSME market was shifting steadily to Tala,Branch etc.. It's a ring fencing strategy.. Not that banks would crumble incase they had continued ignoring the segment I do not use Tala/Branch/MShwari and the such but don't these charge rates of 3-9% per MONTH? The Stawi loans, per the press release, are at 9% per YEAR. That's lower than what they lend to AA customers. I would understand it if banks were charging 3% per month and then taking on more risk. How will banks charge more than the rate cap directive.. The only way is to go lower to stem the tide. MSME have no issue with loans as high as 23% per annum but the law restricts! KCB and CBK loans via MShwari have APRs higher than 50%. The APR includes fees so a facilitation fee of 7% per month is more than 90% APR. Your point? MSME prefers to borrow at 50% than 9%? COOP, IMH, KEGN, MTNU

|

|

|

Rank: Elder Joined: 12/4/2009 Posts: 10,827 Location: NAIROBI

|

VituVingiSana wrote:If the APR is substantially higher than 13%, then is CBK backtracking on its threats that banks should have APRs that were at or lower than CBR+4? 9% interest +4% fee Wealth is built through a relatively simple equation

Wealth=Income + Investments - Lifestyle

|

|

|

Rank: Veteran Joined: 8/28/2015 Posts: 1,247

|

Angelica _ann wrote:JM is aging! In other post .................. https://www.businessdail...4514-vctcsiz/index.html

Probably, he has no yesterday, and his today is messing with the establishment, you ought to know you met us here young boy kinda thing ,Behold, a sower went forth to sow;....

|

|

|

Rank: Chief Joined: 1/3/2007 Posts: 18,390 Location: Nairobi

|

obiero wrote:VituVingiSana wrote:obiero wrote:VituVingiSana wrote:obiero wrote:VituVingiSana wrote:obiero wrote:winmak wrote:Ericsson wrote:murchr wrote:NOTICE - STAWI mobile loan facility of 30 - 250K, payable within 1 -12 months at an interest of 9% per annum Where is equity bank and why have they been left out Unsecured!!! How have they priced in risk to lend at 9%? Or am I missing something? There are huge deposits in banks acrruing 0% interest. That’s your answer Banks can place those funds at much lower risk of default on the Interbank Market. Then there are 91 day T-Bills. Also offer secured overdrafts to existing customers. True. But the MSME market was shifting steadily to Tala,Branch etc.. It's a ring fencing strategy.. Not that banks would crumble incase they had continued ignoring the segment I do not use Tala/Branch/MShwari and the such but don't these charge rates of 3-9% per MONTH? The Stawi loans, per the press release, are at 9% per YEAR. That's lower than what they lend to AA customers. I would understand it if banks were charging 3% per month and then taking on more risk. How will banks charge more than the rate cap directive.. The only way is to go lower to stem the tide. MSME have no issue with loans as high as 23% per annum but the law restricts! KCB and CBK loans via MShwari have APRs higher than 50%. The APR includes fees so a facilitation fee of 7% per month is more than 90% APR. Your point? MSME prefers to borrow at 50% than 9%? @Obiero asked: How will banks charge more than the rate cap directive?

@Obiero said: MSME have no issue with loans as high as 23% per annum but the law restricts!So I ask, if MShwari/Fuliza (CBA and KCB) charge an APR more than CBR+4% why hasn't CBK cracked down on them? Greedy when others are fearful. Very fearful when others are greedy - to paraphrase Warren Buffett

|

|

|

Wazua

»

Investor

»

Stocks

»

Portfolio Balancing: Avoid Over Exposure To Financial Sector

Forum Jump

You cannot post new topics in this forum.

You cannot reply to topics in this forum.

You cannot delete your posts in this forum.

You cannot edit your posts in this forum.

You cannot create polls in this forum.

You cannot vote in polls in this forum.

|